Map")

Solar PV Builds Momentum Across Europe

After years of being labeled a German phenomenon, the solar photovoltaic (PV) sector is building momentum across Europe, particularly in Spain. Catalyzed by newly adopted feed-in tariffs, PV development activity in Europe is booming and project size is scaling - causing shifts in competitive positioning along the project development value chain, according to a recent study from Emerging Energy Research, a leading research and advisory firm analyzing clean and renewable energy markets. After years of dominating the solar PV industry, Germany has been joined by Spain's scaling market and together the two countries are setting the pace for PV development. Spain, Europe's fastest growing PV market, is forecasted to install 800 MW in 2008 and grow to 5.6 GW by 2012, according to EER. With long-term and relatively stable incentive regimes in place, total installed grid-connected PV capacity in Germany and Spain amounted to 1,440 MW in 2007, accounting for 92% of the 1,562 MW installed in Europe.

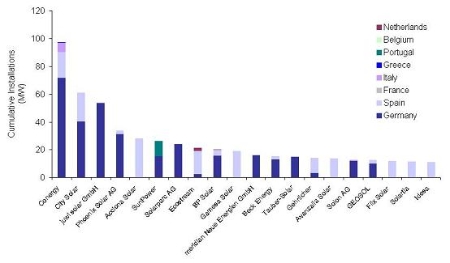

Together, six countries--Germany, Spain, Italy, Greece, France, and Portugal--are expected to hold the lion's share of PV development activity over the coming years by adding 22 GW from 2008 through 2012, according to EER. But the establishment of high feed-in tariffs in emerging markets, including the Czech Republic, Bulgaria, and Switzerland has set off a wave of PV development activity. Developers are now positioning for first-mover advantage to establish operations in these emerging PV markets, according to EER. "The European solar PV market is becoming increasingly fragmented across the value chain from manufacturers to project owners with installers and developers operating in the continuum," according to EER senior analyst Reese Tisdale. Emerging PV-based power producers range from leading renewables utilities to specialized solar PV plant owners looking to gain market share. "As the industry landscape adapts to lucrative feed-in tariffs, new markets, and supply chain bottlenecks, participants are beginning to target segments along the value chain that can leverage their core capabilities in manufacturing, system integration, and project ownership," says Tisdale. German Developers Look to Southern Europe for PV Development With several markets emerging simultaneously and a new focus on Southern Europe, German project developers and investors are expanding their activities beyond their home market to compete in the larger European landscape, according to EER's study. These players must navigate local permitting and feed-in tariff regulations, develop local capabilities, and finance new levels of growth. Leveraging their development experience in the German market and existing vendor relationships, leading German developers including Conergy, City Solar, and Phoenix Solar are now entering Spain, Italy and other Southern European markets to take advantage of feed-in tariff incentives. Leading European utilities--including EDF-EN, Iberdrola, Electrabel, Enel, and Edison--have become increasingly interested in PV. "Given their existing contacts with commercial and industrial clients, and a proven appetite for renewables, European utilities are well-positioned to enter the PV generation market as the sector transitions toward rooftop installations," says Tisdale. Independent power producers, led by Acciona Solar and AES, are looking to continue expanding their renewable portfolios to include solar PV moving beyond wind, solar CSP, small hydro power, and biomass. An emerging group of specialized solar PV power plant producers are also aiming to capture the fruits of their development efforts. These players include Idesa, Renewagy, Solarparc, SunEdison, and S.A.G. Solarstrom. "While the European PV market remains extremely fragmented, in terms of plant construction and plant ownership, emerging players are positioning themselves to be specialized solar IPPs alongside larger renewable players like Acciona or AES," says Tisdale. "For the most part, their strategies leverage their long track record gained in their home markets, secure module supply, and access to capital through financing partners." Supply Chain Challenges Scaling PV Market On the supply side, the pace of technology change and a global shortage in silicon supply have together presented significant challenges to PV project developers and integrators, according to EER's study. New technologies, such as thin film, are driving costs downward and undercutting the traditional silicon based module suppliers. "The downside of rapid growth--typical of such a quickly scaling industry--has been the supply chain's inability to keep pace with demand," says Tisdale. As a result, developers across the value chain have been pressured to secure not only their existing positions but also to switch to less efficient--but less expensive--technology (e.g. thin film), to move toward vertical integration, or to lock in long-term supply agreements to compete more effectively. "To survive the currently evolving market environment, developers' nimbleness will be critical to their ability to keep up with solar PV's increasingly frenetic pace," says Tisdale. ABOUT THE STUDY - SOLAR PV DEVELOPMENT STRATEGIES IN EUROPE 2008-2020 EER's market study, Solar PV Development Strategies in Europe, 2008-2020, released in June 2008, provides comprehensive analysis of PV market activity in Europe with a focus on downstream development activities. The 300-page study profiles leading project developers, supply chain strategies, geographic positioning, and opportunities across 30 countries. Follow this link for the study's Table of Contents and List of Exhibits. For more information please contact Stephanie Aldock at 617-551-8483 or eermedia@emerging-energy.com ABOUT EMERGING ENERGY RESEARCH Emerging Energy Research is a leading advisory and consulting

firm analyzing clean and renewable energy markets on a global

basis. EER is based in Cambridge, Massachusetts and Barcelona,

Spain. Our clients - which include many of the world's largest

energy companies, utilities, technology vendors, and financial

institutions - seek our informed, objective view and advice

on these fast developing markets. For more information visit

www.emerging-energy.com |

Email this page to a friend