Unleashing the Wind TigerJun 22, 2010 - Jackie Jones - renewableenergyworld.com

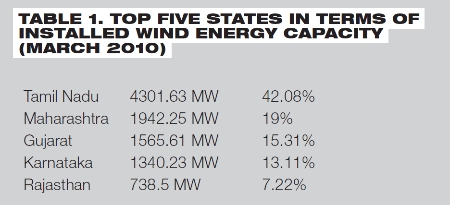

London, UK -- Until China's wind sector started its turbocharged acceleration three or four years ago, India had been the clear leader in wind in Asia and amongst developing countries. A wind pioneer, year after year it has ranked in the top five nations in terms of new installations. India added a respectable 1576 MW during the financial year ending 31 March 2010 (compared with 1917 MW added in Germany and 2459 MW in Spain), bringing total wind capacity to 11,758.43 MW. It is currently in fifth place globally in terms of total installed capacity. The leading state is Tamil Nadu, in the south, which boasts an outstanding level of resource and currently yields about half of India's wind production (see Tables 1 and 2 below), as well as dominating new installations. India's current (11th) Five-Year Economic Plan ends in March 2012, and includes a target of 9000 MW of new wind installations. India's Minister for New and Renewable Energy, Dr Farooq Abdullah, told the Lok Sabha (elected house) that 3847 MW had been installed between the launch of the Plan and end of January 2010. Market analysts predict cumulative capacity in the region of 24–25.5 GW by 2013 (BTM, March 2009) or 2015 (MAKE, March 2010).

India has long had a vision for wind power, and indeed for other renewables. In 1982 the government created a Department for Non-conventional Energy Sources (DNES, given Ministry status in 1992 to become the MNES). Back before carbon-counting, India identified wind power as a means of increasing and securing its electricity supply to a rapidly growing, industrializing nation. In 1985, the DNES initiated a national programme for the development of wind power. The first demonstration projects were built in the late 1980s, joined by the first private sector projects in the 1990s. By 1998, 968 MW had been installed across India, 917 MW of which were put up by the private sector. These machines were in the 200–500 kW range and the developments were largely made possible by finance from IREDA, the Indian Renewable Energy Development Agency. A reduction in tax benefits was followed by a slowdown in developments after 1998. It was a revival of tax-based incentives that saw the sector rebound. Prior to 2003 India's electric power sector – generation and transmission/distribution – was in the hands of the state electricity boards. The 2003 Electricity Act set in motion reforms that have unbundled generation, transmission and distribution in many states, as well as creating Electricity Regulatory Commissions at both state and national levels. With increasing industrialization and a growing population, the country has been facing large outages due to shortfall in power production. India's 11th five-year plan aims to add 78.7 GW of new power generation capacity by 2012 – though in November 2009 minister for power Sushilkumar Shinde warned that India was likely to add only 78% of the 14.5 GW power capacity targeted for 2009–2010. One technology that has exceeded, rather than fallen short of its targets, is wind power. It makes sense that given different incentives, it could deliver much more and become a real contributor to India's energy mix.

(Image, left: India has introduced a number of policy measures designed to boost wind development. Credit: Suzlon) So it should perhaps come as no surprise that the majority of India's wind turbines are also in the category of 'captive power' – built to supply power directly to the owners, typically industrial/commercial enterprises. Danish consultancy BTM has estimated (March 2009) that manufacturing companies generating electric power for their own use make up some 70% of the customers for wind power in India. Modular and scalable, wind generation is in many ways ideally suited to decentralized generation of this kind. It will also have a role to play in rural electrification in India. Wind power's other big strength is in large, utilty-scale, zero-carbon power generation. This is where, despite its positive government stance and early start in wind, India has tended to lag. A new raft of policy measures is designed to give confidence to independent power producers and the investors from the mainstream power industry. Effects of the 'No Hassle' Investment Option The main tool provided by policy up to now has been an income tax-based incentive for investors, known as 'accelerated depreciation'. This allows depreciation benefits of up to 80% of the investment during the first year of the project's operation, meaning that for every thousand rupees invested, 800 rupees can be deducted from taxable income. Investors setting up wind energy projects are also allowed to claim tax exemption for up to 10 years. Alongside this, the Electricity Act of 2003 allowed wind turbine manufacturers to offer investors complete develop-operate-manage packages, with the ownership of specific wind turbines in a wind farm in the hands of investors. This combination has made investing in wind an easy, 'no-hassle' choice for investors in India, assured of generous tax benefits and with all the technical and business practicalities handled by the wind turbine manufacturers. Yet this approach has also meant that the wind sector in India hasn't been attracting investors or developers who are building wind because it makes sound sense in terms of energy or business strategy. The majority are individuals or companies involved in completely unrelated business, making balance sheet investments. According to Ministry of New and Renewable Energy (MNRE) figures, in 2009 independent power producers (IPPs) accounted for just 10% of wind farm investments, while 90% were balance sheet investments. So to some extent the wind power sector has been developing in parallel with the existing power sector, but not as part of it. Further, because wind farm construction has been incentivized, rather than output, efficiencies have not always been a focus. Some might argue that quality has not always been a focus either. So although wind power now accounts for 6% of India's total installed capacity, it only generates 1.6% of the country's power, according to the Indian Wind Turbine Manufacturers' Association. The low overall capacity factor is perhaps due in part to the age of some of the turbines, and their small size. Less-than-optimal siting has sometimes also been an issue. Attracting a New Kind of Investor Against this background, in line with its medium and long-term objectives and under pressure from the wind industry, the government has been looking at measures that will broaden the investor base, incentivize higher efficiencies and output, and encourage the entry of large independent power producers and foreign direct investors to the wind power sector. The introduction of some kind of generation-based incentive has been an evolutionary, rather than revolutionary, process, with developments taking place over the past few years. The State Regulatory Commissions were empowered in 2003 to set tariffs for renewable electricity production, and these have been introduced in several states. For instance, Maharashtra introduced a feed-in tariff for renewables in 2003, Andhra Pradesh and Madhya Pradesh in 2004, Karnataka, Uttaranchal and Uttar Pradesh in 2005. In 2008 Gujarat, Haryana, Punjab, Rajasthan, Tamil Nadu and West Bengal introduced tariffs. Caps range from 50 MW to 500 MW. Gujarat's policy is to target 500 MW in the state, with a feed-in tariff of $0.27/kWh for a period of 12 years. However, these state tariffs, where they do exist, have generally been regarded as insufficient in themselves to encourage a broader spread of investment in wind power. They have been used alongside the existing accelerated depreciation and the other tax incentives. In July 2008 the generation-based incentive (GBI) was also introduced on a pilot basis for new grid-connected plant with minimum size 5 MW. However, the 2008 announcement said that the scheme would be reviewed once 49 MW of new installations had been achieved – making it more or less meaningless considering that 1800 MW of new wind were installed in 2008, and introducing a de facto cap. So perhaps the initial GBI is best viewed as a tactical 'heads up' to the sector that more change was indeed on the way. Meanwhile, also in 2008 a Renewable Portfolio Obligation (RPO) for utilities was being introduced at national level, requiring distribution utilities to purchase a minimum percentage of their portfolio from renewable energy sources. This starts at 5% in 2010, increasing by 1% per year to 15% by 2020. However, the wide differences in geography and wind resource across the country are likely to make it very difficult for some utilities to purchase renewable energy. Commentators were saying it would be very difficult to achieve without some sort of balancing system, such as tradable Renewable Energy Certificates. 'Unlocking the Locks' of Wind Power So, when Minister for New and Renewable Energy Dr Farooq Abdullah said 'we are here to unlock the locks' of wind power in December 2009, he was announcing two refinements to allow existing measures to get off the starting blocks. First, removing the 49 MW cap on the GBI, which is now effectively set at 4 GW. Secondly, the introduction of a mechanism for tradeable Renewable Energy Certificates to kick-start the RPO. The generation based incentive, of 50 paise (just over 1 US cent) per kilowatt hour for a 10-year period, applies only to new grid-connected wind plant, and the installations – minimum capacity 5 MW – must be approved by the relevant utility. There is a cap of Rs6.2 million (62 lakh, US$140,000) per megawatt. The system will be administered by, and financed via, IREDA. This GBI package makes available Rs3.8 billion (US$81 million) until 2012 (for turbines installed up to the end of March 2012), and is planned to support the construction of about 4 GW of new wind capacity within the timeframe. Surely India wants to build more than 4000 MW by then? Indeed it does, but the new incentive does not replace, but supplements, the tax-based incentives. The GBI will be available to investors as an alternative to the existing (and ongoing) programme offering accelerated depreciation tax benefit. Investors will be able to choose which of these two incentives they wish to use, and – importantly – will not be able to switch a project between the two. GBIs already introduced at state level will continue to be available alongside either other benefit. Captive power plants will be able to benefit from the GBI, provided they are grid-connected. The Market's Response to the Measures What the government is clearly trying to do through these latest measures is encourage larger-scale, utility-scale players and installations, so that as well as being a trusted resource for onsite (captive) power, wind power becomes part of the centralized mix. Another objective is to attract foreign direct investment. Will the new measures be sufficient to encourage this new kind – for India – of development? Speaking at a February phone conference hosted by Execution Noble, Ms Namrata Mukherjee – a renewable energy specialist at Mercados in New Delhi – talked about the past frustrations of a situation in which incentives had led 'to lot of capacity coming up but no significant generation contributing to the energy mix of the country'. She also said that since the removal of the 49 MW cap on the GBI 'there is definitely a positive interest within the wind sector community'. It has also captured the interest of the large independent power producers, with IPP scale development now 'coming on board because they do not have to rely on balance sheet kind of funding for setting up these wind power plants ... so it is definitely a positive move.' Mukherjee was also very positive about the tradeable renewable energy certificates, saying that they offered the only way for every utility to meet its obligation by being 'traded irrespective of the electricity component ... as physical certificates.' This again 'is a very positive move and this will attract the genuine investors in the sector.' The question is, when? How long will it take the market to respond to the new environment – in particular, how long for the utilities to start placing orders? According to Namrata Mukherjee it could take 'at least a year ... because only by then can the state regulatory commissions come up with revised obligations for the utilities and then the utilities coming up with their own procedures'. Such market inertia is to be expected – yet the current GBI is due to expire in under two years, though the government has indicated that if the response is positive, the GBI will be rolled on into the 12th Five Year Economic Plan, i.e. beyond 2012. Utilities and investors like long-term clarity. So the sooner an extension of the GBI is confirmed, the better the chance of a positive market response in 2010 and 2011. Also, as the new terms are implemented, there will be some fine-tuning and clarification that will ease uptake. According to T.F. Jayasurya, manager of communication at the Indian Wind Turbine Manufacturers Association (IWTMA), the uptake in growth – albeit just 6.2% in 2009–2010 – is an indicator that India is remerging from recession. He believes the prospects for 2010–2011 are brighter: 'Installations are likely to pick up and we hope to achieve about 2000 MW on the back of a turnaround in the economy and the announcement of the GBI Scheme.' Utilities and Real-time Wind Energy Forecasting Many markets have seen utility resistance to wind power, especially in large quantities. In India, the gap between wind and utilities could hardly have been wider. Do the utilities trust wind power to deliver what they need and not be an unwelcome obstacle in their business? According to IWTMA chairman D.V. Giri, many utilities regard wind power as unstable and infirm. Speaking at Husum Wind in 2008, Giri explained the importance of getting real-time forecasting in place, to enable system operators to plan thermal and hydroelectric outputs around the expected wind output. Accurate forecasting is also essential if generators are to have open access to the electricity markets, as well as power purchase agreements. This is a key concern for developers. The IWTMA selected Garrad Hassan (UK-based but with a Bangalore office), to set up 'real time wind forecasting systems' in two states by April 2010. The systems are being set up in Tamil Nadu and Karnataka, according to IWTMA, but neither the precise locations nor the owners/operators are being revealed. Ramesh Muthya, managing director of Garrad Hassan India, said the forecasting systems would help the system operators plan for other inputs. For instance, 'If six hours before the event, the TNEB (Tamil Nadu Electricity Board) is informed that from a 600 MW installed capacity it is going to get 350 MW of power, it might limit its purchase from the central pool. It might ask the hydropower generators not to exercise their maximum limits.' He explained that every 15 minutes, the forecasting system will generate energy production data for the next 60–72 hours, and present it in two formats – graphical and tabular. Self-correcting intelligence mechanisms will alter the programs according to feeds received from wind farms over a period of time, he said. The Global Industry Boost India has a solid background in wind turbine manufacture, and 3000–3500 MW of new turbines are manufactured each year for home and export markets. As the Indian Wind Outlook (GWEC) points out, about a dozen international companies now manufacture wind turbines in India, through joint ventures, under licensed production, as subsidiaries of foreign companies or as Indian companies with their own technology. As noted earlier, the turbine manufacturers have become accustomed to offering much more than equipment. Some European companies have had a presence in India for years. Vestas, for instance, has a long history in India, through its (earlier) joint venture, Vestas RRB India. RRB is now a separate entity (Vestas Wind Tech was set up when Vestas reorganized after it had merged with NEG Micon). According to BTM's figures, in 2008 Vestas had a market share of 13%, and RRB 9.6%. Enercon has also been in India for some 15 years (Enercon India is a joint venture between the German company and the Mehra Group). Enercon India has several manufacturing plants, offices in over 30 locations, operates in seven states, and employs 3500 staff. Newer to India is Gamesa Wind Turbines Pvt Ltd., of Chennai, a 100% subsidiary of Spain's Gamesa Group. While General Electric did have a presence in India, it reportedly withdrew in 2005 after very poor sales. According to a December 2009 article from Forbes India GE withdrew from the Indian wind market in frustration, saying investors were unwilling to pay the premium for the quality and efficiency they believed they were offering. Now, it appears GE may be back, with reports of a new manufacturing plant opening later this year. However, the out-and-out market leader in India for some eight years is Suzlon. Set up in 1995, Suzlon has grown not only in India but internationally, finding its way into the rankings of the global top five manufacturers. It has struggled financially over the past year or two, but in India, Tulsi Tanti's Suzlon had a market share of 50%+ in 2008 and 2009. Will India's new incentives attract a rush of new players to its wind sector? It may not be a stampede, but recent announcements suggest that more leading manufacturers have an eye on India – especially those who have a track record of selling other, non-wind, power equipment to the IPP/utility sector. Perhaps Suzlon's financial woes have alerted others to an opportunity, and perhaps those others see India as a sound base from which to serve the broader Asian market. The Indian government may not have firmed up its long-term policy incentives for wind power, yet there are plenty of positive signals. Jackie Jones is consulting editor to Renewable Energy World, e-mail: rew@pennwell.com.

Sidebar: Indian Industry Announcements September 2009: Reports that GE will open a wind turbine manufacturing plant during the second half of 2010, most probably at a south Indian location, to commence production of 300 of GE's 1.5 MW machines per year. Then president and CEO of GE India, Tejpreet S. Chopra, is reported as saying 'what's very encouraging is the fact that the government's moving from the tax-incentive/tax-depreciation methodology of providing incentives to more generation based incentive programme.' February 2010: Siemens unveils its plans to open a €70 million (US$98 million) 200 MW wind turbine production facility in India. The facility will be commissioned in 2012, and may eventually be expanded to 500 MW. February 2010: Spanish wind turbine manufacturer Gamesa announces it has started operations at its new wind turbine factory near Chennai, producing 200 MW per year of its 850 kW machines. Run by Gamesa's new Indian subsidiary, Gamesa Wind Turbines Pvt Ltd, the new plant adds to its Asian production capacity of 1 GW per year from installations in China. Gamesa said it will support the new facility with 'the ongoing development of local suppliers for the supply of components and materials.' April 2010: Bharat Heavy Electricals Ltd (BHEL) announces it is planning to re-enter wind turbine manufacturing in the next three months, in cooperation with a foreign technology partner. BHEL used to manufacture 250 kW wind turbine generators but discontinued due to a fall off in demand. Now, the company says it is looking at manufacturing 1.5 – 2 MW machines. The unit's existing fabrication facility will be used to manufacture towers and nacelles, while it will take another two years to set up a wind blade manufacturing facility near the existing unit in Ranipet.

|

India has featured as one of the world's top five countries for wind power development for years. Will new policy initiatives open up India's wind sector?

India has featured as one of the world's top five countries for wind power development for years. Will new policy initiatives open up India's wind sector?  So what's to unlock? In spite of the impressive progress, India's wind sector has developed almost in isolation from the wider power sector, and the wind industry has lobbied hard for policy measures that would open the way for larger-scale wind farms and attract new investors, including international capital.

So what's to unlock? In spite of the impressive progress, India's wind sector has developed almost in isolation from the wider power sector, and the wind industry has lobbied hard for policy measures that would open the way for larger-scale wind farms and attract new investors, including international capital.

With per capita consumption of electricity in households low, the industrial sector is one of the largest consumers of electrical energy in India. A number of industries rely increasingly on their own sources of power generation rather than on grid supply – either because an adequate grid supply is not available, or because the grid supply is unreliable, or because the electricity tariffs make so called 'captive power' generation advantageous. Various estimates over recent years have said captive power makes up 20%–25% of the total installed power capacity in India.

With per capita consumption of electricity in households low, the industrial sector is one of the largest consumers of electrical energy in India. A number of industries rely increasingly on their own sources of power generation rather than on grid supply – either because an adequate grid supply is not available, or because the grid supply is unreliable, or because the electricity tariffs make so called 'captive power' generation advantageous. Various estimates over recent years have said captive power makes up 20%–25% of the total installed power capacity in India.